(ゲームにはまりつつも、ながらでブログもちゃんと書きます。)

ADP社は世界110か国、65万社の顧客に対して給与計算などの人事関連のアウトソースサービスを提供する企業です。

創業は1949年と古く、パンチカード式の計算機によるサービスから始まって、現在に至るまで人事サービス一本で成長してきました。買収もたくさん行ってきています。

顧客企業にとって、人事関連サービスは本業とは関係のないものの、なくてはならないサービスです。自らの手でやるよりも、プロにお任せしてしまった方が安くつく種類の業務です。しかも、その費用は全体の利益からすれば大した額ではなく、サービスの質がよほど悪くなければ他社に乗り換える動機も少ないと考えられます。つまり、「顧客にとって取るに足らないコストに過ぎず、乗り換える手間を躊躇させる」タイプの参入障壁を持っていると考えられます。

米国内での競合にはPaychex社(PAYX)がありますが、売上で1/4程度であり、顧客企業の規模による棲み分けをしているようです。

決算情報を見てみます。なお、ADPは6月決算です。

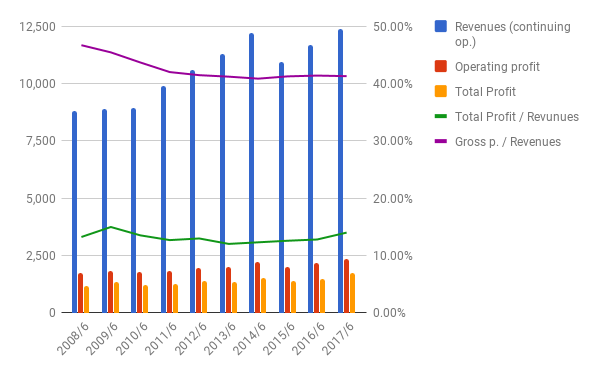

売上・利益

成長はほぼ止まっているようですが、利益率は悪くないですね。

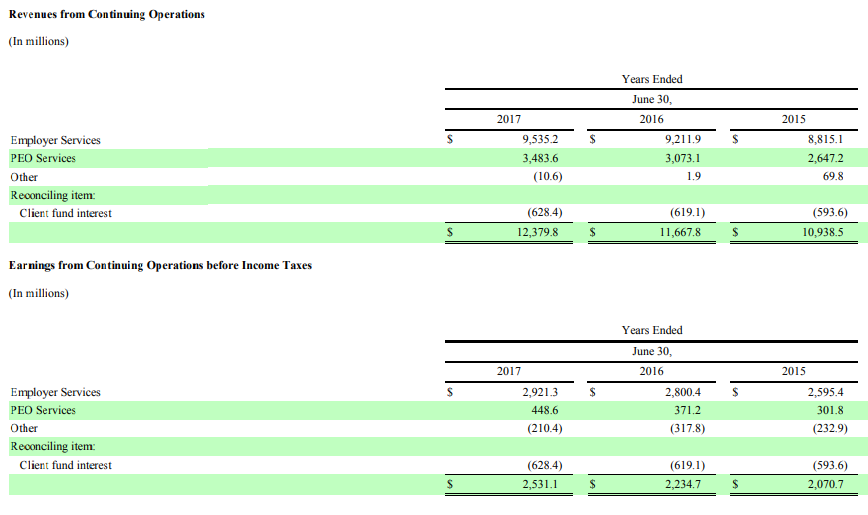

セグメント

一番売上の多い”employer services”というのは、給与、福利厚生、人材マネジメント、保険、退職、税金関連といった一連の人事関連サービスのことです。利益率は30.6%です。

“PEO services”とは、習熟作業者の派遣サービスです。利益率は12.9%です。

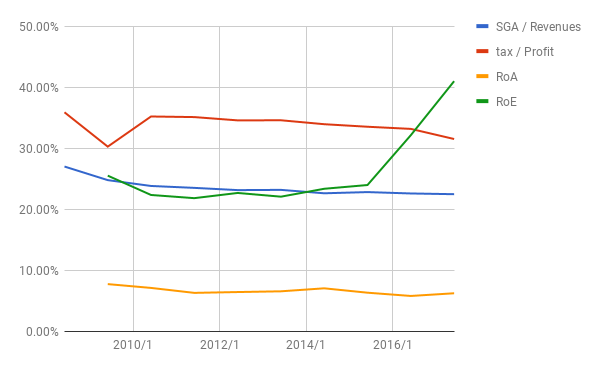

比率

ROEが急増していますが、これは後述するように分母つまり資本が減っているためです。

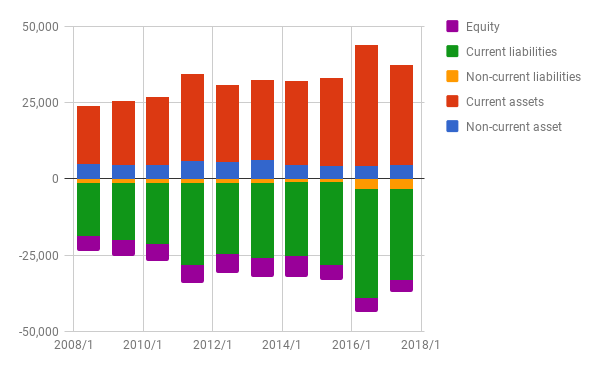

バランスシート

おおむね問題はなさそうです。

なお、資本は、2015/6年の4.809M USDから、2017/6には3,977 M USDへと、約17%減っています。これは、自社株買いによるものです。よい傾向です。

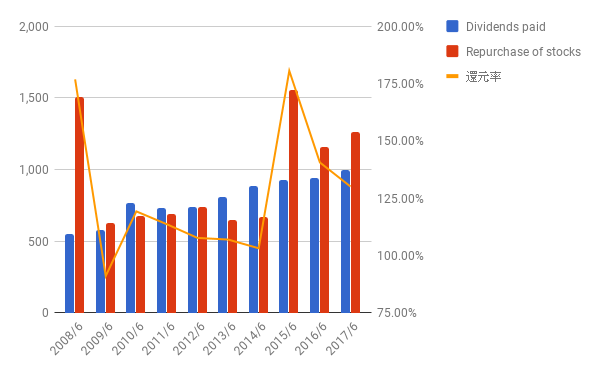

株主還元

配当と自社株買いにより、ほぼ毎年100%を超える還元を行っています。徹底的に株主に報いています。

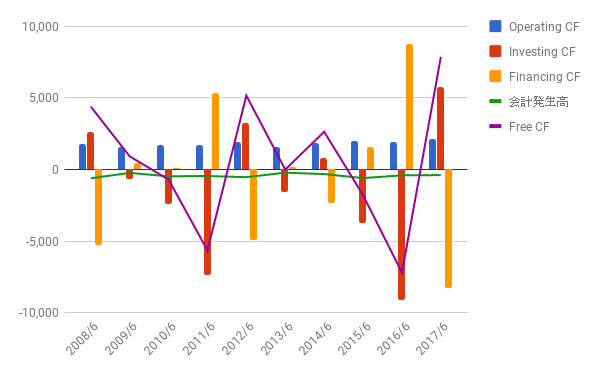

キャッシュフロー

営業CFは安定していますが、投資CFと財務CFが凸凹です。しかし、それぞれプラスマイナスでほぼ帳消ししている感じですね。

財務CFは、プラスの年もマイナスの年も、その大部分を”Net (decrease)/increase in client funds obligations”が占めています。

一方で、投資CFにもそれに見合うくらいの額の”Net decrease/(increase) in restricted cash and cash equivalents held to satisfy client funds obligations”という費目があります。

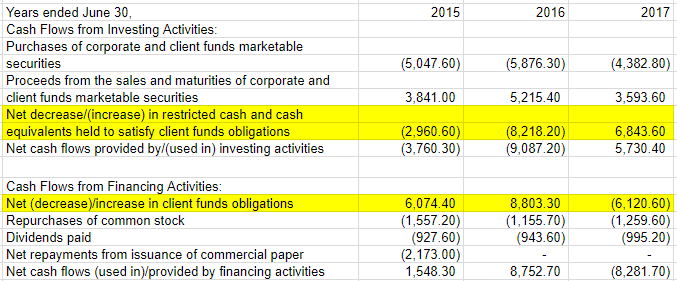

CF抜粋(2015/6~2017/6):

これらについての説明は、決算書に以下のように書かれています。

Client funds obligations represent the Company’s contractual obligations to remit funds to satisfy clients’ payroll and tax payment obligations and are recorded on the Consolidated Balance Sheets at the time that the Company impounds funds from clients.

The client funds obligations represent liabilities that will be repaid within one year of the balance sheet date.

The Company has classified funds held for clients as a current asset since these funds are held solely for the purposes of satisfying the client funds obligations.

The Company has reported the cash flows related to the purchases of corporate and client funds marketable securities and related to the proceeds from the sales and maturities of corporate and client funds marketable securities on a gross basis in the investing section of the Statements of Consolidated Cash Flows.

The Company has reported the cash inflows and outflows related to client funds investments with original maturities of ninety days or less on a net basis within net increase in restricted cash and cash equivalents and other restricted assets held to satisfy client funds obligations in the investing section of the Statements of Consolidated Cash Flows.

The Company has reported the cash flows related to the cash received from and paid on behalf of clients on a net basis within net increase in client funds obligations in the financing section of the Statements of Consolidated Cash Flows.

要は、顧客から預かった給与や税金といった一時的なお金を、投資CFや財務CFに参入しているとのこと。長い目で見れば、無視してもよいものだと思います。

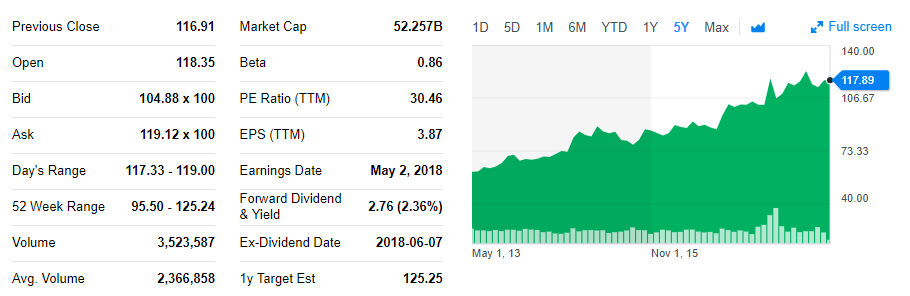

株価

5年チャート:

PERは30.46。「安い」とは言えないと思いますが、5年チャートを見てわかるように、押し目らしい押し目はありません。今後もおそらくそうでしょう。

株価は、配当を無視してもこの5年で2倍になっています。2.76%の配当の再投資を考慮すればもっと高いリターンがあるでしょう。

現在の強固な参入障壁が維持される限りは、持っておいて損はない銘柄でしょう。

ITの進歩が激しい現在、どこの異分野から見知らぬライバルがやってくるかもしれません。しかし、そのリスクは、加工食品会社が抱えている消費者の健康志向や小売りのプライベイトブランドによるリスクに比べれば、小さなものだと考えます。前者はあくまで潜在的リスクですが、後者はすでに顕在化しているリスクです。

よかったら押してください。